|

| [Actual St. Paul rental data! -- see link at the bottom.] |

I've heard from folks who have been watching the entire proceedings, but I want to highlight just a few of the talks that I've found the most informative. Check them out for sure if you have any interest in learning more about this complex topic.

For example...

Aeon Expert on the Need for Market-Rate Housing

I was riveted by this 40-minute presentation on the big picture of St. Paul affordable housing from Sarah Harris, who works at Aeon, the largest housing preservation non-profit in the area. They're the ones that desperately tried to save the St. Anthony Village trailer park, and the folks there spend almost all their time and energy preserving naturally-occuring affordable housing (NOAH). In other words, they're well-versed in the pros and cons of different policies around local housing.

I was riveted by this 40-minute presentation on the big picture of St. Paul affordable housing from Sarah Harris, who works at Aeon, the largest housing preservation non-profit in the area. They're the ones that desperately tried to save the St. Anthony Village trailer park, and the folks there spend almost all their time and energy preserving naturally-occuring affordable housing (NOAH). In other words, they're well-versed in the pros and cons of different policies around local housing. Here's what Harris says about the scale of the housing crisis and why government is not going to solve this problem (anytime soon):

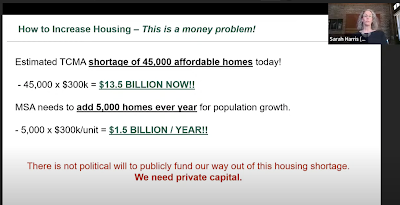

It costs about $300,000 [to build a home], probably more given the way construction costs are rising, but let’s just say $300,000. Whether it’s affordable housing or market-rate, it’s the same cost.To acquire and rehab NOAH units, it’s about half that, or $150,000.It takes 2-4 years to build a new unit of housing, and 3-5 years to build new affordable housing (it takes longer because the funding cycles are that much more complicated and competitive). And yet we are losing NOAH properties because it only takes about 3 months for those buildings to be acquired and lost.In Ramsey County, it was stated that 37,000 families live below the 30% AMI level, and they need about 15,000 new units of affordable housing. Well you multiply 15,000 by $300,000 and that’s $4.5 billion that we need right now to serve Ramsey County’s need.The county recently announced a $74 million funding pool. That’s a lot of money, but not even a drop in the bucket relative to the need. And that doesn’t even account for the ongoing and increasing demand, which you can see the chart on the right. It shows that the city of St. Paul has an increasing population every year since 2010, and with the need now and the losses we are experiencing, that does not even account for the fact that our demand is growing because the population is growing.So that’s Ramsey County. Let’s extrapolate it over the entire metro region, and we have a shortage of 45,000 affordable housing units today. At $300,000, that’s $13.5 billion that is needed right now to put those units in place. Plus we need 5,000 homes every year just to account for population growth. 5,000 new units at 300K would be another $1.5 billion per year and that’s not even accounting for the losses of NOAH, which are around 6,300 units per year.So that’s another $9 billion if we were to build our way out of those units we were losing. If we were to preserve them its still $1 billion to keep those units affordable housing.When you start looking at numbers of this magnitude there’s not the political will, and importantly there’s not public funds available, to pull us out of this housing shortage. We are needing, and will always need, private capital to help solve this issue.

Harris goes on to explain why and how private housing investors make decisions, and the importance of keeping yield high enough to attract investors. The whole talk is great, especially if you want a cogent development and housing 101 explainer.

I'll also recommend the talks by rent policy researcher Ken Baar (from this meeting) who talked about the intricate history of rent control regulations in the US, and Rasheedah Phillips of Policy Link (immediately preceding Sarah Harris) who gave an overview of the housing affordability crisis in the US. In each case, the experts offered a nuanced, detailed perspective of policies like the one currently on the books in St. Paul.

The ULI / Fed Talks are Even Better

For example, there's a great ongoing series on rent stabilization and housing that's being put on by ULI Minnesota and the Minneapolis Federal Reserve. They've organized an ambitious four-part series on rent stabilization policies, bringing in an impressive group of national experts. For example, Part One included Ed Goetz from CURA, Jenny Schuetz from

Brookings (who I spoke with last year), people from the Fuhrman Center (ditto). They all mostly agreed that the issue is complicated and we need a "both/and" solution, though did not explicitly discuss the St. Paul example.

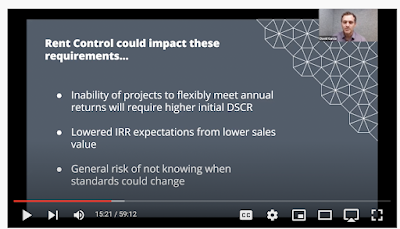

Part Two was even more interesting to me. I especially enjoyed the talk by David Garcia, who is the policy director for the Terner Center at the University of California-Berkeley. He gave a very detailed explanation about how development financing works, and why rent control reduces housing construction. Indeed, it's the most coherent explanation of this difficult issue that I've yet seen (and I've heard a lot of them).

Here are the key points, from about 14:00 into the presentations:

So how could rent control impact these [development] requirements?So in a rent control regime where new construction might not be exempt from controls, that would create an inability of projects to flexibly meet their annual returns. And from a bank’s perceptive, they’re going to assess that as a risk. And they may require an initial higher debt-service coverage ratio, which may be beyond what the developer can demonstrate they can handle. And in those instances, it’s likely that the project just doesn’t work.And so even if a pro forma, which is how developers calculate their returns, indicates a 3% increase per year, that [seems] pretty conservative and it doesn’t seem like rent control could impact that…

But that’s an average. So if there’s a recession, and there are 2-3 years (or less than that) where they can’t actually meet that 3% goal, but then coming out of a recession they’re not allowed to go higher than that... Well a bank’s going to judge that as too risky. And again they may not provide a loan to that project.Also there could be lower IRR (internal rate of return) expectations from lower sales at the back end of the project itself. So if there is an expectation that rents have to stay constant or at least controlled through a rent stabilization ordinance, that lowers value at the end, it lowers IRR expectations and maybe they’re not as attractive to the investor themselves.So even if a developer can demonstrate that there is strong rent growth, even in the presence of rent control, a private investor may still bake in some of that risk to their IRR calculations. And they decide not to provide financing to that project.

If you're interested in housing and rent policy, I cannot recommend these talks highly enough. It's a great resource, and there are two more yet to come from the ULI/Minneapolis Fed in the next few weeks.

Shane Phillips Discusses Rent Stabilization Tradeoffs

He dove into the rent stabilization policy debate around the 35:00 mark, where he discussed the problem with "stability-only" policy approaches. Here Phillips is commenting directly on the existing St. Paul ordinance:

It’s understandable that people assume that, because so many issues in America really do come down to wealth inequality, housing must be the same. But the truth is that we have both a redistribution / inequality problem and we have a quantity / supply problem. And we have to address both. One or the other isn’t going to cut it.Some quick examples on how this stuff links together: Let’s say you’re considering rent stabilization, which I hear St. Paul has done recently, and made some bad choices perhaps. If you’re considering this though, how should you design it?If you only care about stability — and [for] the recent ballot initiative, this might describe it pretty well — you could cap rent increases on every unit, including new ones, and keep those caps [in place] even between tenancies. The result, which we’ve seen all across the world when you do these things, is that new development will be much riskier. And rents on existing units will fall relative to the cost of operating them, and you’ll end up with fewer apartments getting built, and more apartments getting converted into condos.So now you’ve got low rents on more units, but you’ve got fewer of those units every year, and the ones that become available probably aren’t going to be going to the people with the greatest need. They’re going to go to family friends. They’re going to go to people willing to pay key money. They’re going to go to small households that don’t have kids, because the landlords think that larger households might cause more damage to the unit.In some sense this kind of approach is just trading one kind of decline for another. Instead of prices rising too quickly, which is bad, you have a dwindling stock of poorly maintained homes.And I think we can do better than that. I don’t think it’s inevitable that those outcomes come to pass. Suppose instead you take supply into account when you’re thinking about the stabilizing policy [side] of rent stabilization. You can design the policy to do some very basic things.Exempt new buildings for the first twenty years, for example, and allow apartments to reset to market rates when units turn over. The result from this is [that] tenants in older, more affordable units will still have that security and predictability, but homes continue to get built because developers can still make their profits when it matters. And fewer rentals get converted to owner-occupancy because eventually the tenants move out, and you’ll be able to go back to market rate, and it works fine.This isn’t the maximal approach where every existing tenant gets everything they could possibly want, but it’s balancing short-term and long-term interests, and providing security to the people that need it most, which should be our priority.

The rest of the talk is good too, especially if you haven't read his book or listened to his podcast from the UCLA Lewis Center.

PS. Finally Some Data

And as a special bonus, Tony Damiano at CURA has compiled actual St. Paul rent history for us (about 20:00 in), something I've been wanting to see for many months. Check out the presentation here, or skim the slides here.